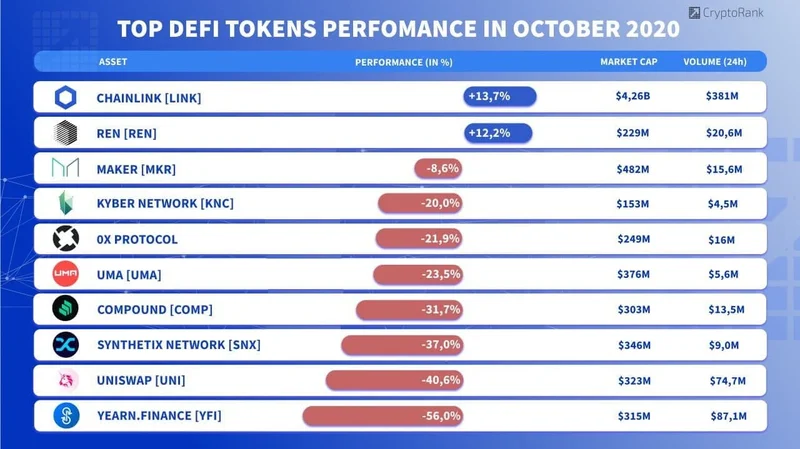

The DeFi Mirage: Why "Safer" Isn't Always Safe

The crypto market's post-October 10th crash aftershocks continue to ripple, and the decentralized finance (DeFi) sector is feeling the tremors. FalconX's recent report paints a bleak picture: as of November 20, 2025, only a sliver—2 out of 23—of leading DeFi tokens are in the green year-to-date. Quarter-to-date, this cohort is down an average of 37%. That's a bloodbath by any standard.

The "Safety" Illusion

The report suggests investors are flocking to "safer" names, specifically those with buyback programs. HYPE (down 16% QTD) and CAKE (down 12% QTD) are cited as examples of larger market cap names posting relatively better returns. But let's unpack this "safety" narrative. A buyback program, in essence, is a company using its own funds to repurchase its shares (or, in this case, tokens). The idea is to reduce supply, theoretically driving up the price. But a buyback is only as good as the underlying asset. If the fundamental value is eroding, a buyback is just delaying the inevitable, like rearranging deck chairs on the Titanic. The question isn’t whether a token has a buyback, but why it needs one. Is it because organic demand is lacking? Is it a sign of desperation, not strength?

I've seen this pattern play out countless times in traditional finance. A company announces a massive buyback, the stock price jumps, and everyone cheers. But six months later, the company is still struggling, and the buyback is revealed as a short-term gimmick to boost executive bonuses. Are we sure something similar isn't happening here?

Then there’s the "fundamental catalysts" argument. MORPHO (down 1% QTD) and SYRUP (down 13% QTD) outperformed their lending peers due to "idiosyncratic catalysts." Minimal impact from the Stream finance collapse, or growth in other areas. Okay, but idiosyncratic means unique. It's not a repeatable strategy. It’s luck, or at best, skillful navigation of a specific crisis. You can't build a portfolio on idiosyncratic events. It’s like saying you’re a successful gambler because you once won a hand of blackjack.

The Great Valuation Reset

The FalconX report highlights a shifting valuation landscape. Spot and perpetual decentralized exchanges (DEXes) have seen declining price-to-sales (P/S) multiples, as prices fell faster than protocol activity. This makes sense. A lower P/S ratio can indicate undervaluation, but it can also signal that the market has reassessed the growth potential of these DEXes. Some DEXes, like CRV, RUNE, and CAKE, posted greater 30-day fees as of November 20 compared to September 30. This is interesting, but it doesn't tell the whole story. What's the trend? Is this a temporary blip, or a sustained increase in activity? The data point alone is meaningless without context.

Lending and yield names, on the other hand, have broadly steepened on a multiples basis, as prices have declined considerably less than fees. KMNO's market cap, for example, fell 13% over this period, while fees declined 34%. This is a red flag. It suggests that investors are clinging to these tokens despite deteriorating fundamentals. The report suggests investors are "crowding" into lending names, viewing them as "stickier" than trading activity. Maybe. Or maybe they're just bagholders in denial, hoping for a rebound that never comes. (The parenthetical clarification: I’ve seen this exact dynamic in distressed debt funds.)

The report further posits that this positioning reflects investor expectations for DeFi sector growth in 2026. Perps are expected to lead the DEX front (HYPE’s outperformance), while fintech integrations will drive growth in lending (AAVE, MORPHO). Perhaps. But that assumes these expectations are rational. And in the crypto market, rationality is often in short supply.

And this is the part that I find genuinely puzzling. Why would anyone expect "perps on anything" (HYPE's HIP-3 markets) to be a sustainable growth driver? It sounds more like a recipe for regulatory scrutiny and market manipulation. And fintech integrations? That's just traditional finance creeping into DeFi, which kind of defeats the whole point.

It all boils down to this: are investors genuinely assessing the long-term viability of these DeFi protocols, or are they simply chasing the next shiny object, hoping to ride the wave before it crashes? The data, frankly, suggests the latter.

Fear-Driven Flight

The relentless sell-off has undoubtedly shaken investor confidence. Andy Baehr's "Vibe Check" in the FalconX report notes "sentiment is max negative," with many caught off guard by the recent leg down. He quotes Eric Peters, who aptly states, “There are more sellers than buyers." Obvious, perhaps, but profoundly true. And that’s when it's time to be careful.

Baehr also mentions that "big wallets" that may have sold above $100k appear to be buying back 20% lower. This is a classic "buy the dip" strategy, but it doesn't guarantee a rebound. It just means that some whales are betting that the market has bottomed out. They could be right. Or they could be adding fuel to a dead cat bounce.

Baehr's conclusion is that a trend overlay can help "smooth the ride" and keep investors in the game. That's a reasonable strategy for long-term investors. But for those chasing quick profits in the DeFi space, it's like putting a band-aid on a broken leg. The underlying problem remains: the fundamentals are shaky, the valuations are inflated, and the "safer" bets may be the riskiest of all.

Data-Driven Delusions

The Solana (SOL) analysis doesn't offer much comfort either. Sure, Solana boasts impressive throughput (1,000+ transactions per second) and low transaction costs. Its ecosystem is expanding, and staking rewards are enticing. But the article itself acknowledges that SOL's price is heavily influenced by Bitcoin and Ethereum trends, macroeconomic conditions, and regulatory developments. In other words, it's subject to the same f